Simple Budgeting Tips to Save More and Spend Smarter. Money savings don’t need to be difficult! By adding these simple hacks into your daily routine, you can reduce expenses, boost savings and achieve financial success more quickly.

Begin by reviewing both your income and outgoings. Making adjustments to recurring expenses such as dining out and subscription fees can make an immediate impactful change.

1. Set Goals

Make budgeting part of your everyday routine through consistency. Once you develop the habit, spending less than you make will become much easier and opening your bank statement will become an enjoyable experience.

Start by tracking your expenses for several weeks, noting every purchase and expense – from coffee and household items, cash tips, and regular monthly bills, right down to coffee tips and cash tips you receive – from using simple spreadsheets or free budgeting apps online, such as Mint or pen and paper! Be sure to include both recurring and non-recurring expenses, debt repayment or savings goals set as you go along.

Start by calculating your take-home income and then creating an expense list of essential (rent, utilities) and non-essential expenses (food, entertainment). Knowing your needs makes setting aside money easier each month; but before getting started set some short-term savings goals as this may provide motivation to stay on your savings journey.

2. Automate Your Savings

Manage your money can become a challenging balancing act when bills and expenses mount up, especially if you’re trying to save for something in particular. But saving more and spending smarter doesn’t have to mean giving up things you enjoy doing.

One effective strategy to do so is automating your savings, meaning a portion of each paycheck is directly transferred into an investment or savings account on a regular basis. Doing this helps eliminate the need to think about saving and overcome mental blocks like “I’ll save later”.

Transferring money between accounts can be done manually or using budget apps; alternatively you could link both savings and checking accounts together so funds can easily transfer between them.

Start an emergency fund, invest in your retirement, or use this to reach other financial goals you have for the future. Use it to pay off credit cards or cancel subscriptions you no longer require such as streaming services, coffee shop memberships or app purchases that you no longer use – any way it suits you best!

3. Prioritize Your Expenses

No matter your level of experience with budgeting, it’s essential to keep a broad picture in mind when creating or adapting a budget plan. Too often we hear generic advice like “save more and spend less” that doesn’t take account of each unique circumstance.

Prioritizing expenses allows you to make smarter financial decisions by relieving stress and aligning spending with goals. Furthermore, regular reviews of expenses allow you to adapt your budget according to current needs and goals.

Begin by compiling all of your income and expenses. This should include everything from your monthly pay check, tips and credit card purchases. Be sure to include expenses from sources such as retirement or savings accounts as well as benefits, debt repayments or pensions that come regularly into your life. Once you’ve recorded all your spending, prioritize it by categorizing needs versus wants; needs include essentials like food and shelter while wants could include things such as streaming subscriptions or shoes on your wishlist.

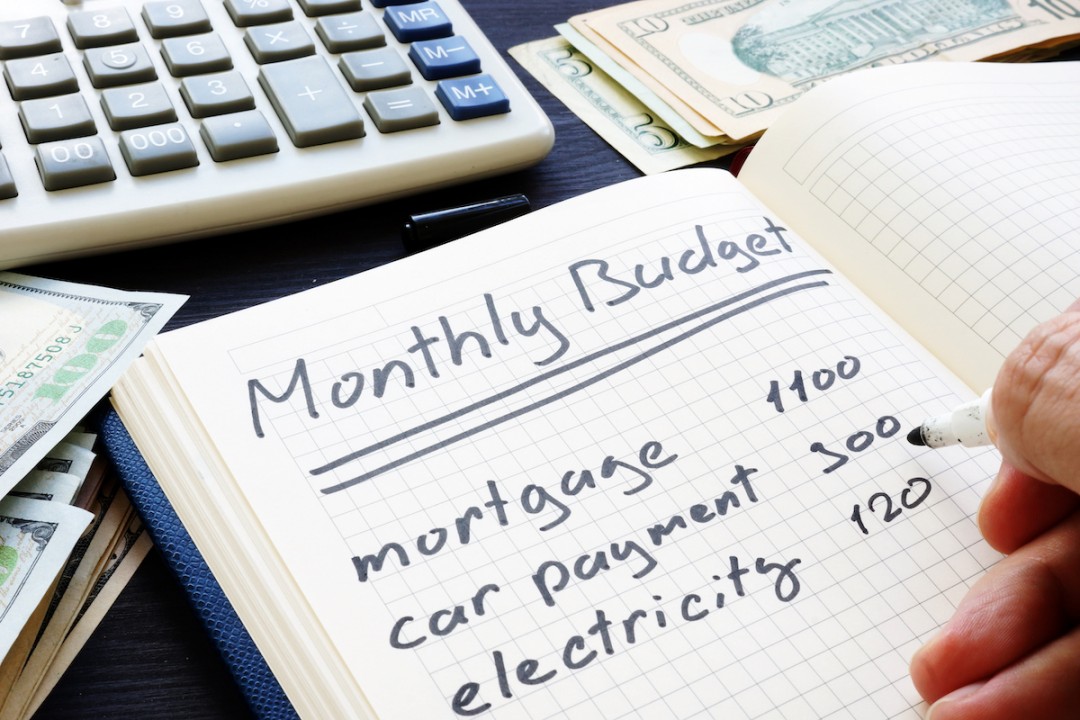

4. Set a Budget

Handling money can be a difficult and delicate balancing act, especially when bills pile up and paychecks stretch too thin. A budget is an effective way to help stay on top of finances. Begin by writing down your take-home income, followed by writing down and calculating all fixed expenses such as rent/mortgage payment, groceries and debt payments, entertainment/coffee subscription costs and dining out expenses as variable expenses (and be sure to include an allowance for savings goals!). A spreadsheet or app such as EveryDollar/Mint will make this much simpler!

Once you understand your spending and savings habits, review them to identify areas for potential reduction. Consider whether each purchase meets an immediate or long-term need. Keeping financial goals in mind can help prevent impulse buys while saving more in the process – eventually leading to more savings, lower debt levels and an improved sense of financial management – it might take practice but will more than pay off!

5. Set a Goal for Your Emergency Fund

Though unexpected expenses are unavoidable, having an emergency fund can ease both stress and financial strain. Financial experts suggest saving enough to cover three to six months’ essential living expenses in case something comes up unexpectedly.

Calculate an ideal savings amount by reviewing monthly bills, credit card debt and other fixed expenses; subtract any discretionary spending such as dining out, subscription services and entertainment from this total; then set an achievable savings goal and start automating contributions to an independent savings account.

Make savings a part of your routine by setting up automatic transfers from your checking account each month, treating it like an ongoing bill payment. This can help build emergency savings steadily while remaining out of sight and mind.

Use any windfalls such as tax refunds, work bonuses or cash gifts to increase your savings, such as tax refunds, bonuses or gifts of money. Be mindful in how you utilize these resources – such as tax refunds, bonuses or cash gifts. Reevaluate your emergency savings target as your income or financial responsibilities change; consider moving it into a high yield account so you get maximum return for your money; increase monthly contributions so you’re closer to creating an emergency cushion!